This program trading use case is for portfolio managers, asset managers, and institutional traders looking to achieve Best Execution when offloading or onloading new assets in bulk. It demonstrates how to leverage advanced, automated strategies to trade entire baskets of securities with maximum efficiency and minimal market impact and it illustrates the complete workflow—from creating a basket of orders and selecting an optimal execution strategy, to monitoring its performance in real-time.

Example Use Case: Choosing the Right Program Trading Strategy

The primary challenge for traders is executing a basket of orders to achieve a specific portfolio-level goal. Unlike single-stock trading, the focus is on the collective performance of the basket. Here are four common scenarios:

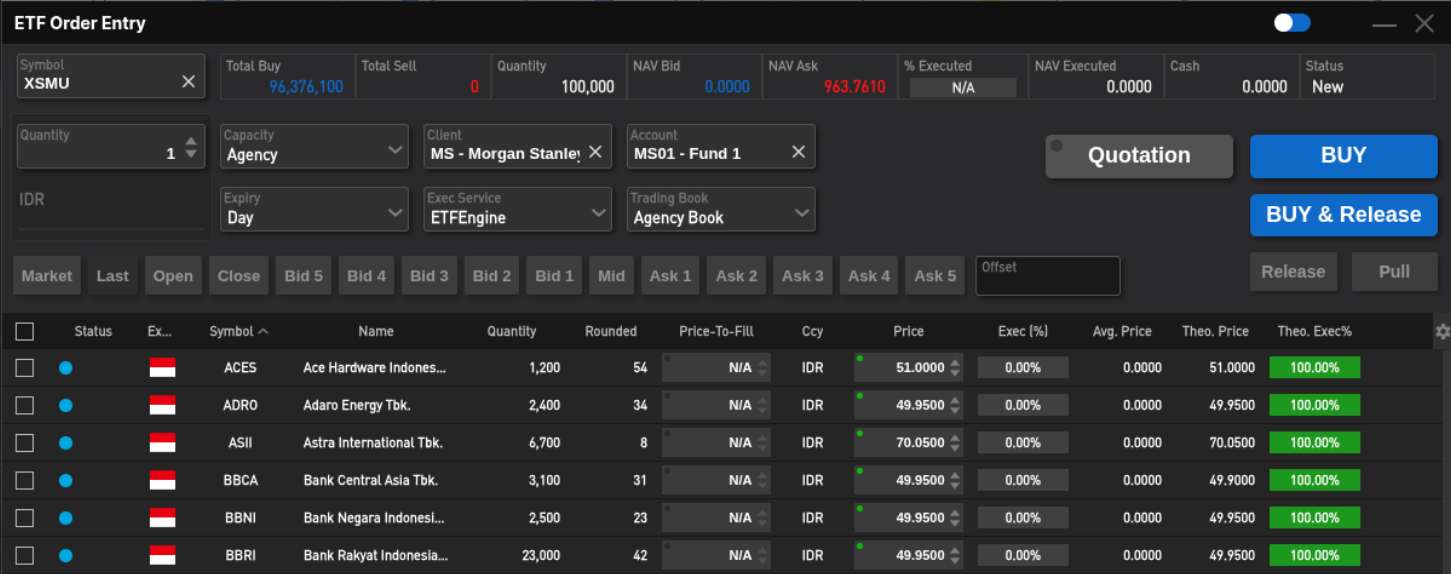

Use Case 1: ETF Creation/Redemption

- Scenario/Goal: An ETF issuer needs to perform a daily creation operation, buying a precise basket of 500 underlying securities to create new ETF shares. The execution must be completed by 3:00 PM with minimal tracking error against the benchmark prices.

- Recommended Strategy: A Program Trade with a VWAP (Volume-Weighted Average Price) algorithm applied across all child orders.

- Why it Works: Using a VWAP strategy for the entire creation basket ensures that execution is paced evenly throughout the day, minimizing the market impact of each individual trade. This disciplined approach is critical for achieving a final portfolio price that is closely aligned with the daily benchmark, which is essential for accurate ETF pricing.

- Marvelsoft Program Trading Advantage: Before committing the basket to the market, you can perform powerful pre-trade analytics. This involves running a theoretical execution simulation against current market conditions to forecast potential market impact and costs, allowing you to refine your strategy for optimal results before placing a single order.

Use Case 2: Automated Sector Rotation

- Scenario/Goal: A quantitative fund’s model has signaled a rotation out of the Technology sector and into the Healthcare sector. The goal is to execute this 200-stock basket (selling 100 tech stocks, buying 100 healthcare stocks) as a single, automated event.

- Recommended Strategy: A Pairs/Spread Trading Program that links the sell-side of the basket to the buy-side.

- Why It Works: This strategy treats the entire rotation as a single transactional unit. The program can be configured to execute legs simultaneously or maintain a specific value neutrality, ensuring the rotation doesn’t expose the fund to unintended market risk. By automating the execution, the fund can act on its signal instantly and systematically.

Use Case 3: Agency Program Execution for a Client

- Scenario/Goal: A sell-side agency desk receives a large “Not Held” basket order from a major client to be worked over two days. The client’s mandate is to beat the arrival price benchmark while not exceeding 15% of the volume in any single stock.

- Recommended Strategy: A Program Trade using a TVOL (Target Volume) algorithm with a hard limit on the participation rate and a multi-day execution window.

- Why it Works: This strategy provides the flexibility needed for a “Not Held” instruction. The TVOL algorithm allows the desk to participate naturally with market volume, while the hard participation limit ensures the client’s constraint is never breached. The multi-day setting allows the program to be paused at the end of Day 1 and seamlessly resumed on Day 2, providing full control and adherence to the client’s mandate.

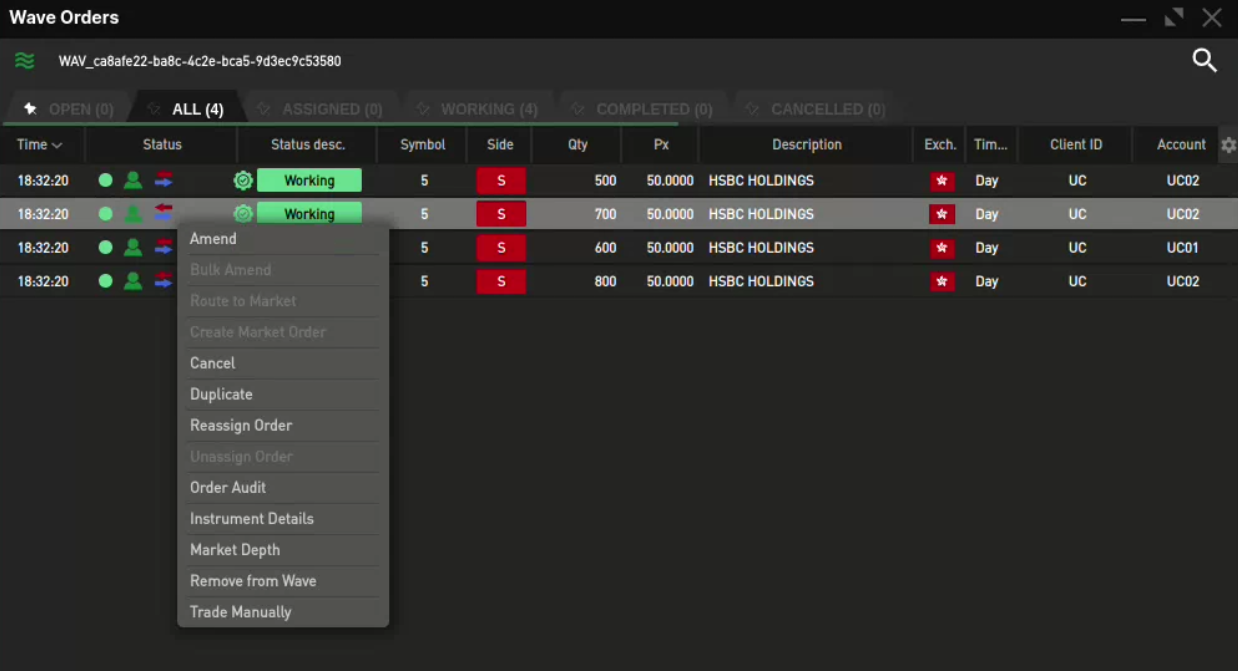

- Marvelsoft Program Trading Advantage: For traders who want to apply their market intuition with surgical precision, the platform offers a powerful Wave Trading feature. This allows you to break down the main program trade into smaller, child baskets (waves) that can be released to the market manually. It provides the perfect blend of automation and discretion, enabling you to time your executions based on real-time market conditions and your expert judgment.

Use Case 4: Automating Basket Execution via Scheduled Events

- Scenario/Goal: A portfolio manager needs to execute a small rebalancing trade on a specific set of stocks every day at 10:00 AM. The process is repetitive, and the goal is to automate it completely to reduce operational overhead.

- Recommended Strategy: A Scheduled Program Trade configured via the basket execution interface.

- Why it Works: The platform allows a fully configured basket—including the instruments, quantities, and chosen execution algorithm—to be saved as a template and scheduled for automatic release at a specific time each day. This “zero-touch” workflow completely automates recurring trades, ensuring disciplined execution without requiring any manual intervention from the trader.

Best Practices or Tips: SME Commentary

The Art and Science of Basket Trading: Beyond the Algorithm

Executing a basket of securities is far more complex than trading a single stock. While algorithms are critical, a successful program trade requires a holistic, portfolio-level approach. We asked our CEO, Matija Maretic, for his perspective.

“Anyone can bundle a list of stocks and hit ‘execute.’ The real value is unlocked when a trader can dynamically manage the program’s internal logic in response to live market events. For example, what if one stock in your basket suddenly faces a liquidity crunch? Our platform allows a trader to see that leg is lagging and instantly switch the algorithm for just that one stock—maybe from a passive VWAP to an aggressive SNIPER—without ever disrupting the rest of the program.

It’s about giving traders the power to react to micro-level events within a macro-level strategy. That’s the difference between simple execution and achieving the best execution.”

Overview of the Product: The Program Trading Platform

Our Program Trading platform is an advanced solution designed to give traders and portfolio managers a decisive edge when executing complex, multi-leg orders. At its core, the platform is built for:

- Precision and Control: The platform is engineered to manage market impact across a basket of securities, minimize tracking error against a benchmark, and execute large, complex strategies with minimal slippage.

- Flexibility in Strategy: It supports a wide array of program trading scenarios, including pairs trading, ETF creation, and fully automated scheduled trades.

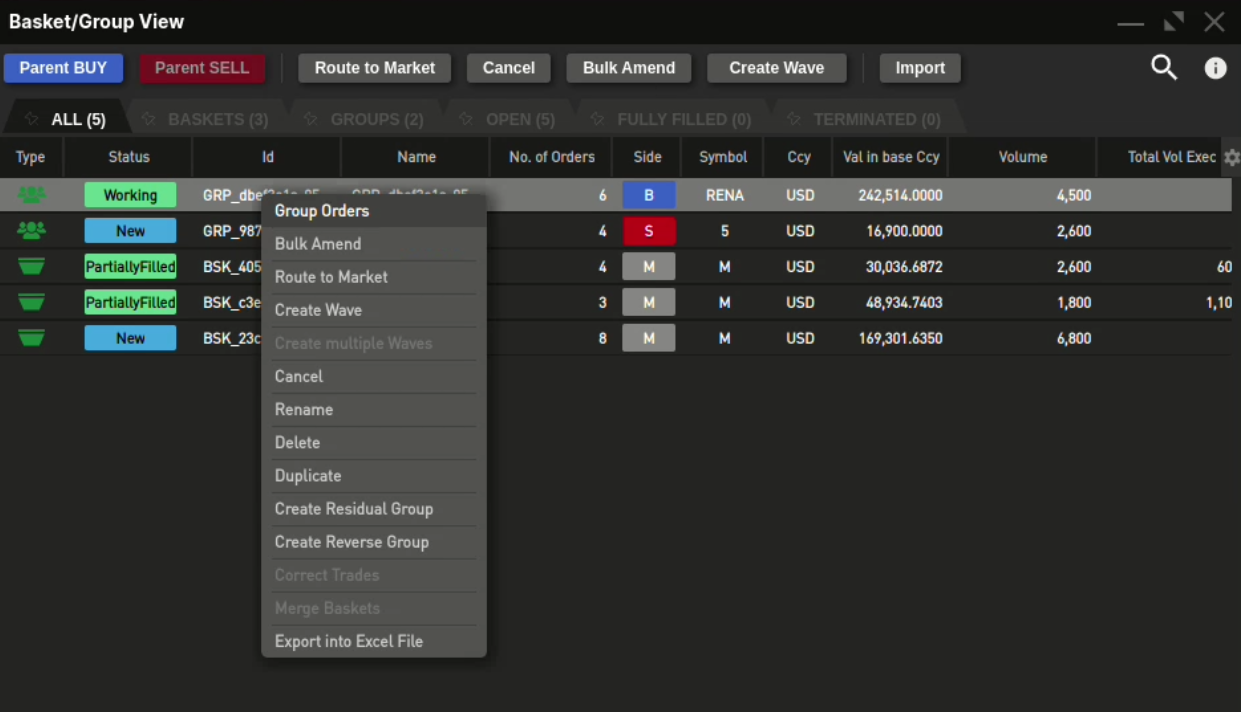

- Seamless Integration: The system allows for easy basket creation—manually, via file upload, or through schedulers—and is fully integrated with our advanced Execution Algo Suite for child order execution.

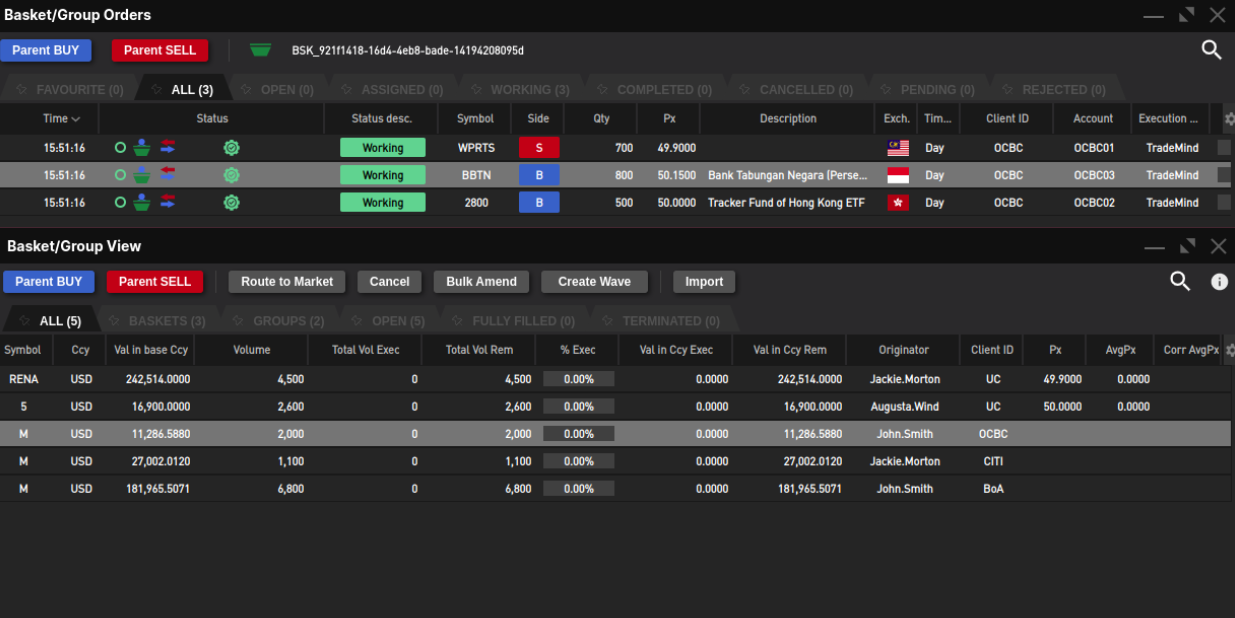

Step-by-Step Guide: Automating Basket Execution

The Program Trading workflow is streamlined into four key phases, accessible directly through our platform’s dedicated Program Trading View.

Phase 1: Order List Import and Profiling

- Access the View: Navigate to the main application toolbar and select the Program Trading module.

- Import the Basket: Import the list of orders (the “basket”) via a standard file upload (e.g., CSV). The system automatically parses symbols, quantities, and side (Buy/Sell).

- Weighting and Allocation: Review the system’s initial weighting, which can be based on market value, volume, or custom parameters. Adjust the distribution or define constraints (e.g., maximum market impact allowed per stock).

- Pre-Trade Review: The system performs initial compliance checks and pre-trade analysis on the basket, providing immediate feedback on estimated market impact and liquidity profiles for all components.

Phase 2: Execution Strategy and Parameterization

- Select the Primary Strategy: Define the overall execution goal for the program (e.g., execute 100% of the basket by end-of-day, minimize deviation from a benchmark, or prioritize speed).

- Assign Algorithms: The system allows for bulk assignment of an execution algorithm (e.g., VWAP, TWAP) to all components. Alternatively, you can use the Dynamic Algo Wheel to automatically assign the optimal algorithm for each individual stock based on its profile (liquidity, volatility).

- Set Global Controls: Define high-level risk and execution limits that apply to the entire basket, such as maximum price deviation or an overall program ‘kill switch’ threshold.

- Define a Wave Strategy (Optional): For very large programs or to strategically time execution, you can configure a Wave Strategy. This allows you to break the basket’s execution into distinct phases (e.g., a “morning wave” and an “afternoon wave”). Each wave can be configured with its own unique start/end times, quantity percentage, and even a different primary algorithm, providing an additional layer of strategic control over market impact and information leakage.

Phase 3: Launch and Real-Time Monitoring

- Release the Program: Once fully parameterized and reviewed, click Release Program to send the entire basket for execution. The program begins slicing and submitting child orders via the assigned algorithms.

- Monitor Progress: Use the Program Trading View to monitor the execution of the entire basket in real-time. Key metrics include:

- Program % Filled: Overall progress toward completion.

- Basis Point Deviation: Real-time performance against the chosen benchmark (e.g., Arrival Price or VWAP).

- Component Status: Granular tracking of fills, remaining quantity, and individual performance for every stock in the basket.

- Intervene: The view provides tools for real-time control, allowing traders to pause the entire program, manually adjust parameters for specific components, or activate a granular Kill Switch on components deemed high-risk.

Measuring Success: Analytics for Program Performance

Analyzing a program trade requires a portfolio-level perspective. Our integrated Transaction Cost Analysis (TCA) toolkit allows you to measure performance against your basket-level objectives.

- For the ETF Creation Use Case (VWAP): Your primary metric in the TCA report would be Tracking Error vs. the VWAP benchmark for the entire basket. A low value confirms the program successfully minimized costs and stayed close to the target.

- For the Sector Rotation Use Case: Success is measured by analyzing the Spread Slippage; the difference between the basket’s value at the time of the order and the final executed value.

- For the Agency Program Use Case (TVOL): You would analyze the Participation Rate to confirm you stayed within the client’s limits, and check the execution price against the Arrival Price benchmark to prove performance.

Conclusion

The Marvelsoft Program Trading platform provides portfolio managers and traders with the precision, control, and analytical feedback required to achieve Best Execution for their multi-leg strategies.

By leveraging the right strategy for your specific objective—whether rebalancing a portfolio, automating a strategy, or servicing a client—your team can consistently optimize performance and gain a decisive competitive advantage.

Ready to streamline your portfolio execution? Contact our experts today for a detailed demo and see the Program Trading platform in action.